A module to perform DCCA coefficients analysis. The coefficient rho describes the correlation strength between two time-series depending on time scales. It lies in [-1, 1], 1 being perfect correlations, and -1 perfect anticorrelations.

The package provides also functions returning a 95% confidence interval for the null-hypothesis (= "no-correlations").

| Travis |

|---|

|

The implementation is based on Zebende G, Et al. DCCA cross-correlation coefficient differentiation: Theoretical and practical approaches (2013), and was tested by reproducing the results of DCCA and DMCA correlations of cryptocurrency markets (2020) from Paulo Ferreira, et al.

To compute DCCA coefficients, call the rhoDCCA function like: pts, rho = rhoDCCA(timeSeries1, timeSeries2). It has the following parameters:

rhoDCCA(timeSeries1, timeSeries2; box_start = 3, box_stop = div(length(series1),10), nb_pts = 30, order = 1)Input arguments:

- timeSeries1, timeSeries2 (Array{Float64,1}): Time series to analyse, need to be of the same length.

- box_start, box_stop (Int): Start and end point of the analysis. defaults respectively to 3 (the minimal possible time-scale) and 1/10th of the data length (passed this size the variance gets large).

- nb_pts (Int): Number of points to carry the analysis onto. mostly relevant for plotting.

- order (Int): Order of the polynomial to use for detrending. If not given, defaults to 1 (linear detrending). If

orderis too high, overfitting can happen, impacting the results.

Returns:

- pts (Array{Int,1}): List of points (time-scales) where the analysis is carried out.

- rho (Array{Float64,1}): Value of the DCCA coefficient at each points in

pts.

As a rule of thumb : values of rho in [-0.1,0.1] usually aren't significant.

The confidence intervals provided by this package correspond to the null-hypothesis i.e no correlations. If rho gets outside of this interval it can be considered significant.

To get a fast estimation of the confidence interval, call the empirical_CI function like: pts, ci = empirical_CI(dataLength).

For a more accurate estimation, you can call bootstrap_CI: pts, ci = bootstrap_CI(timeSeries1, timeSeries2; iterations = 200). This operation can be much more demanding (a few minutes). The iterations argument controls the number of repetitions for the bootstrap procedure, the higher the value, the smoother and cleaner the estimation will be, but it will also take longer.

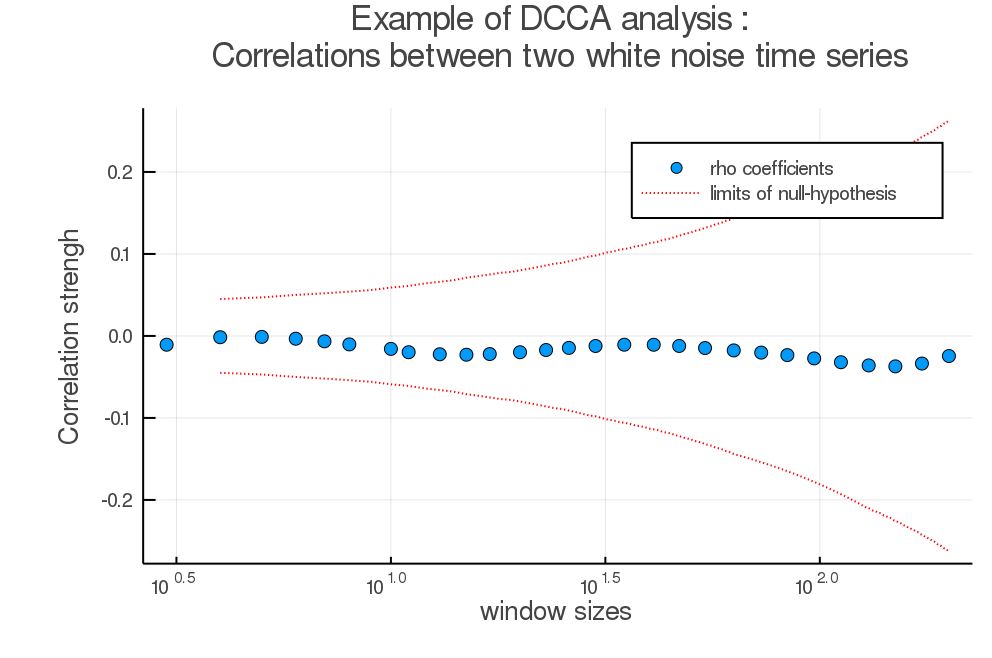

Calling the DCCA function with random white noise

julia> ts1 = rand(2000)

ts2 = rand(2000)

x, y = rhoDCCA(ts1, ts2)

pts, ci = empirical_CI(length(ts1))Gave the following plot :

a = scatter(x,y, markersize = 7, xscale = :log, title = "Example of DCCA analysis : \n Correlations between two white noise time series", label = "rho coefficients", xlabel = "window sizes", ylabel = "Correlation strengh")

plot!(a,pts,ci, color = "red", linestyle = :dot, label = "limits of null-hypothesis")

plot!(a,pts,-ci, color = "red", linestyle = :dot, label = "")

display(a)

julia> Using Pkg

Pkg.add("DCCA")- implement spline detrending?